Some Highlights

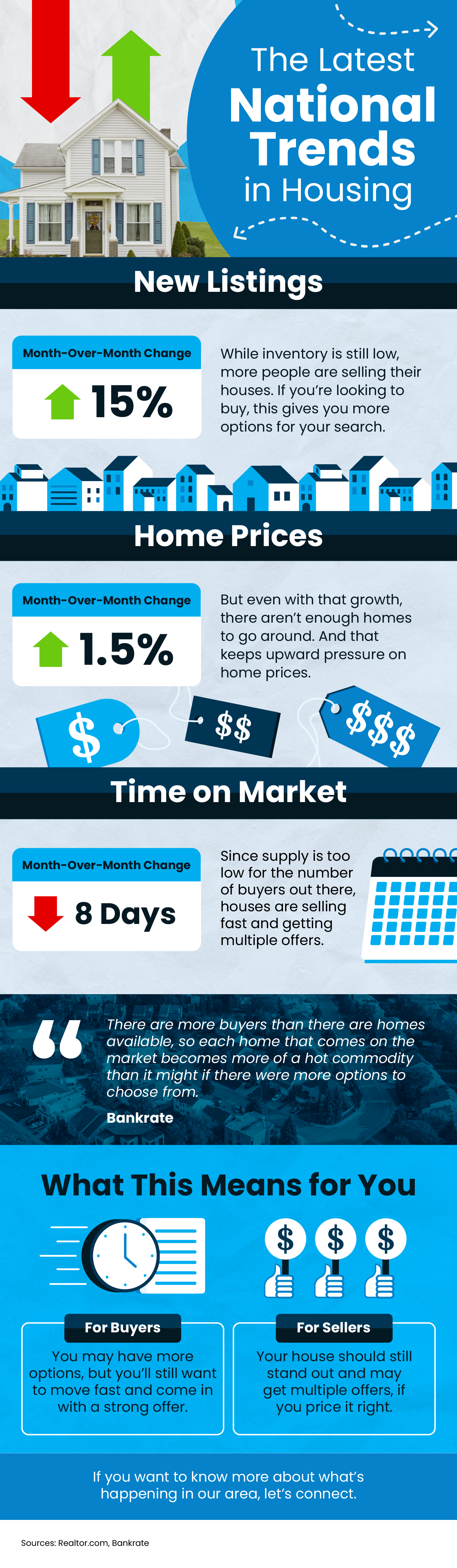

- With the number of new listings going up and average days on market going down, buyers may have more options, but will still want to move fast.

- For sellers, inventory is still low and houses are selling fast, meaning your house should stand out and may get multiple offers if you price it right.

- If you want to know more about what’s happening in our area, let’s connect.